Rebuilding Your Credit Score It Takes Time, but Borrowers Can Improve Their Credit

During the housing boom that lasted from about 2001 through much of 2006, mortgage lenders gave out loans to just about anyone who applied. Or at least it seemed that way. Maybe that’s why the national home ownership rate soared to 69 percent as late as 2006, according to the U.S. Census Bureau.

It turned out that many of those mortgage loans that lenders passed out during the boom were suspect. RealtyTrac, an online provider of real estate data, said that housing foreclosure filings reached 2.3 million in 2008. That’s an increase of 81 percent from 2007, and an all-time high. Many of these foreclosures are a direct result of mortgage lenders passing out home loans to people whose financial situations should have precluded them from ever taking on the responsibility of owning a home.

Mortgage Lenders More Cautious Today

Today’s mortgage lenders are a lot more cautious about who they approve for mortgage loans. During the heyday of the housing boom, even borrowers with suspect credit — not to mention high levels of debt and shaky job histories — were able to obtain mortgage loans with low interest rates.

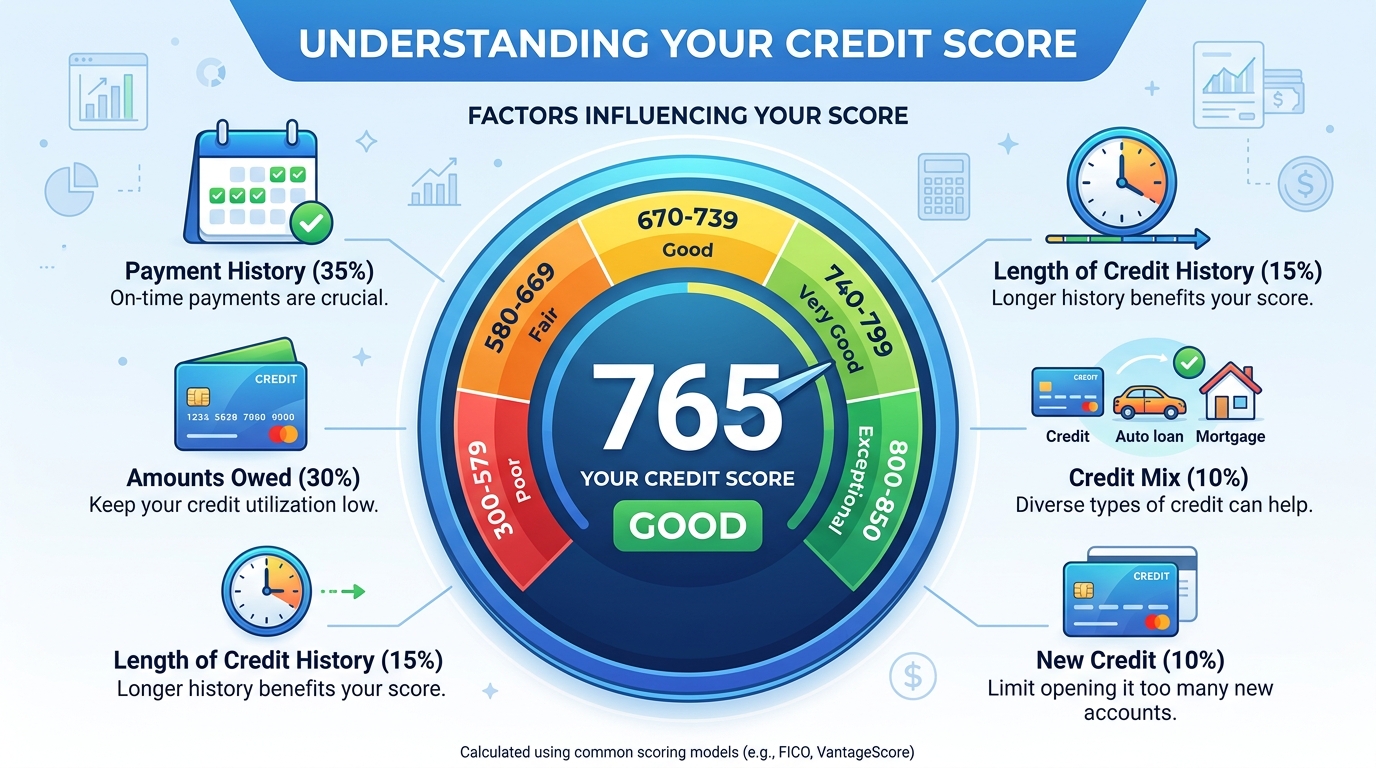

Today, though, borrowers must have solid credit if they hope to qualify for a mortgage loan. Credit scores have long been king in the world of mortgage lending. These scores are numbers — with 700 and up ranking as excellent — that try to distill exactly how much of a credit risk a borrower is. Today, mortgage lenders want to work with borrowers who have strong credit scores. Those who don’t either won’t qualify for a loan or will have to pay higher mortgage interest rates to offset the risk that they’ll default on their loans.

What can borrowers do if their credit scores aren’t the strongest? There may not be need to panic. Borrowers can rebuild their credit scores. It will take time, but it can be done.

A Rebuilding Project

As a first step, borrowers should order copies of their credit reports from the country’s three credit bureaus: Experian, Equifax and TransUnion. Borrowers can do this for free by visiting AnnualCreditReport.com, a Web site that is owned jointly by the three credit bureaus. The credit bureaus occasionally make mistakes. If borrowers find a mistake on their report, they should immediately take the steps to correct it. Unfortunately, this takes a fair amount of time, so borrowers should make sure to check their credit reports well before they’re ready to start applying for mortgage loans.

Another way for borrowers to improve their credit scores is to pay down or, better yet, eliminate their credit-card balances. According to the Federal Reserve, the average household in this country now struggles with an average credit-card debt of $8,700. Borrowers with this much credit-card debt will certainly lower thier credit score.

No Quick Path to Boosting a Credit Score

Borrowers must pay all their bills on time, too. Late payments are the most common reason why people are saddled with bad credit scores. Borrowers who consistently pay thier bills on time will see their credit scores rise.

Unfortunately, there is no quick remedy for a poor credit score. All of these fixes take time. Borrowers simply can’t turn bad credit scores into good ones in a day, no matter how many roadside signs promise that they can. For some borrowers, this may mean a wait of a year or more to buy a home. Buyers, though, shouldn’t view this as a negative. They should instead consider it a chance to rebuild their credit scores and improve their financial stability at the same time. Those potential buyers who do both of these will truly be ready to become homeowners.